With the goal of expanding access to homeownership, Trump posted on Truth Social with a graphic showing "Great American Presidents," including Franklin D. Roosevelt, whose New Deal housing reforms helped pave the way for the modern 30-year mortgage, and himself, suggesting he will develop a 50-year version.

“A Financial Frankenstein’s Monster”

Long ago, 30-year fixed-rate mortgages were described as “a financial Frankenstein’s monster” from the perspective of lenders.

And while the history is fairly complicated, 30-year mortgages essentially date back to the Depression era. Fundamentally, 30-year mortgages are a government invention.

The government-sponsored enterprises Fannie Mae and Freddie Mac purchase mortgages from private lenders, allowing them to offload the risks associated with lending large sums of money for long periods of time (at a fixed interest rate).

Some believe that the government’s support is what made 30-year mortgages a legitimate option, and ultimately led to their sustainability and popularity. But could that future be guaranteed for the 50-year mortgage?

Looking at the Numbers

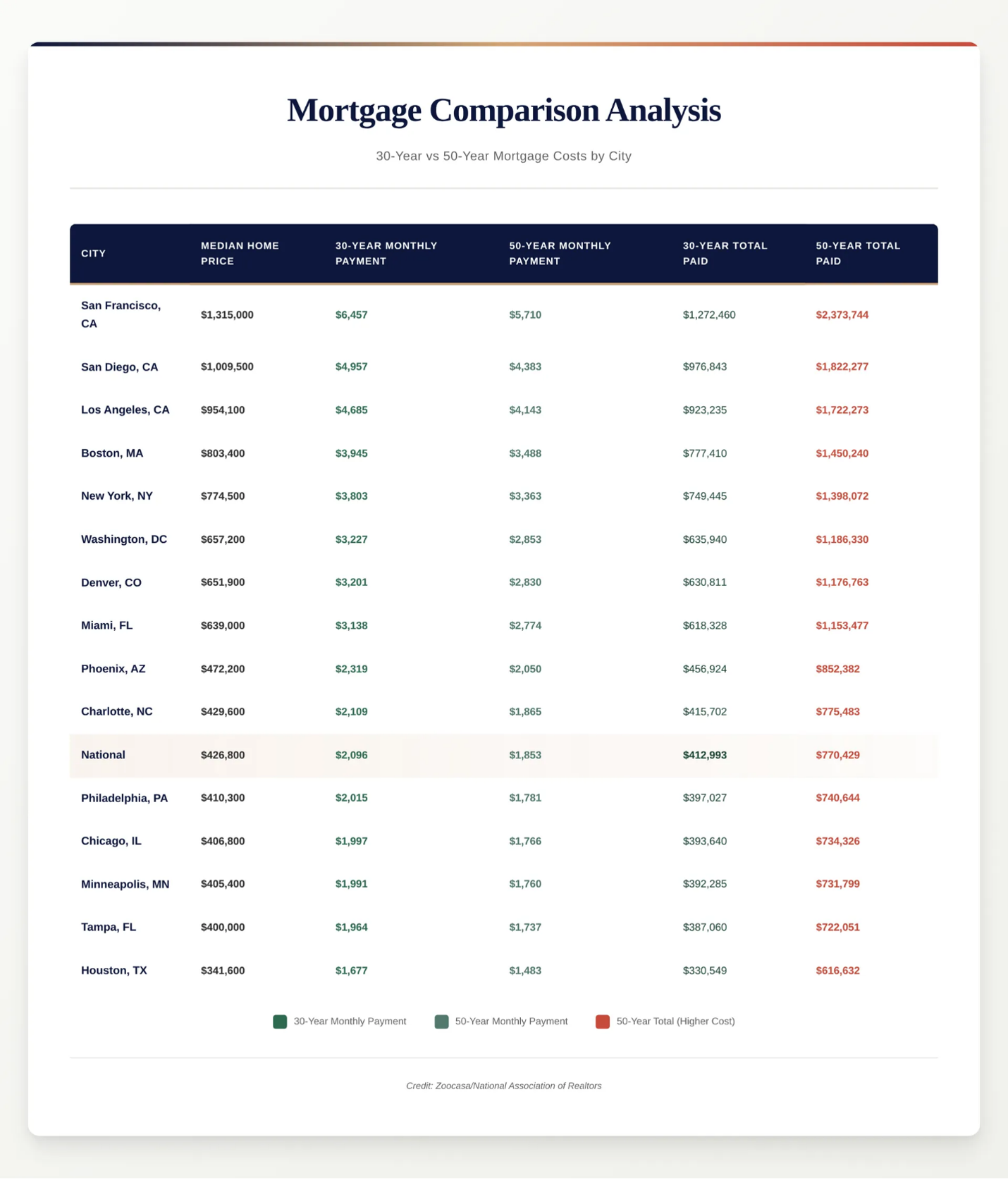

A UBS analysis found that a 50-year mortgage results in total interest payments equal to roughly 225% of the home’s price, which is more than twice the level under a 30-year loan.

UBS also noted that with a 50-year term, borrowers would have paid down only about 11% of the principal after 20 years, highlighting how slowly equity builds over such an extended period.

The length of the 50-year loan makes it riskier for banks, which would likely raise interest rates, as well.

Better Solutions May Lie on the Supply Side

Regardless, there is still one critical issue when it comes to housing affordability — the lack of supply of homes.

States like California and cities like New York have recently passed legislation and regulatory changes to allow builders to build homes faster with less red tape.

And there’s still the raw cost of homebuilding to consider.

Products such as steel, lumber, concrete, copper and plastics that go into home construction are now subject to tariffs under President Trump. Further, many construction jobs were being done by undocumented workers, particularly in the Southwest, where deportations are impacting the ability for homebuilders to find enough labor to build homes.

So, before long-lasting, significant change can be made within the housing industry, the argument can be made that we need to get better at increasing (and maintaining) our supply levels first.

“You Can’t Take Your Mortgage With You If You Sell Your House”

Unlike many other countries, in America, you can't take your mortgage with you if you sell your house. So when people sell their house and move, they end their mortgages. And that plays an important role in dissecting the potential reality of 50-year mortgages.

The typical American homeowner spends less than 12 years in their home, according to a recent Redfin analysis of the U.S. Census data. And that's actually high compared to recent history. Back in the early 2000s, Americans typically spent around seven years in their homes.

Daryl Fairweather, chief economist at Redfin, believes that:

"...most people will not have that 50-year mortgage product for that length of time... I think in a world where this product exists, a lot of people might sign up for it initially and then try to refinance later."

One benefit that would be true for 50-year mortgages, as is the case with all fixed-rate mortgages, is the ability to freeze rates and then refinance later if the opportunity arises is a huge benefit to homebuyers. It offers predictability on your housing costs. And, especially nice, a fixed-rate mortgage basically shields you from inflation and its accompanying higher interest rates.

The Bad and The Ugly of Long-Term, Fixed-Rate Mortgages

Any long-term, fixed-rate mortgages come with costs: they tend to have higher interest rates than adjustable rate mortgages and you have a longer period upfront paying interest and not actually paying down your loan much. But that fact is amplified when you apply it to a 50-year timeline.

If the housing market gets dicey and prices start plummeting, having a large outstanding loan at a fixed interest rate could create serious problems.

Long-term, fixed-rate mortgages increase the probability that you can go underwater on your home, a situation where you owe more on your house than it's worth.

So, if you sell, it means the money you get won't cover your debt. It gets much harder to refinance, meaning you're stuck with a higher interest rate than you could otherwise get in a situation where the housing market tanks.

Not an ideal situation, especially if we speculate on broad-term adoption of 50-year mortgages.

Closing Thoughts

Our top priority is to educate and empower our clients. While the 50-year mortgage is currently nothing more than spirited speculation, products such as 30-year fixed and adjustable-rate mortgages are alive and well.

Informed decisions are strong decisions. At The CL Team, we’re here to help you before, at, and far beyond the closing table to build concrete strategies for one of the biggest investments of your life.

If you’re ready to purchase or refinance your next home, don’t hesitate to give us a call or visit us online today.

Discover more articles.

Stay informed with more of our informative blog posts.

.png)

.png)